Punch line: the current “FANGAM” out-performance falls shy of the pace and magnitude recorded during this stage of the epic 2015 “FANG” run.

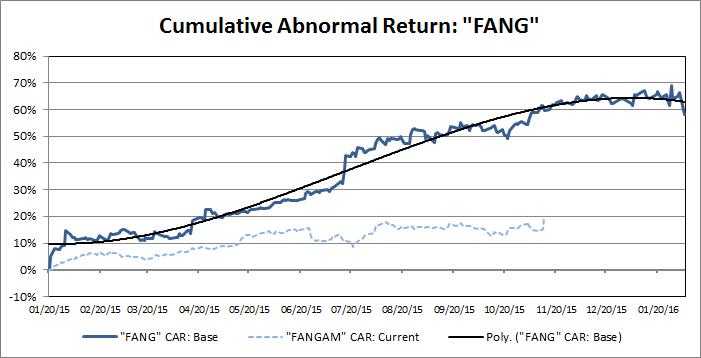

Give the current hype surrounding “FANGAM” stocks (FB, AMZN, NFLX, GOOGL, AAPL, MSFT) I revisited an earlier expose, “Anatomy of a crowded stock,” which illustrated the 2015 relative performance of FANG stocks as a poster-child specimen of the life-cycle dynamics of crowding. The 2015 cumulative abnormal return (“CAR”; summation of daily beta-adjusted excess return; Jan 20, 2015 – Feb 5, 2016) of FANG stocks is depicted in the chart below (lighter dashed line is the current 2017 YTD FANGAM CAR):

Next, I superimposed the current CAR of FANGAM stocks, component and aggregate, around the fitted value of the 2015 FANG CAR, which serves as a baseline boundary threshold, to help contextualize their YTD out-performance. Inter-temporal relative-valuation dynamics notwithstanding, the current FANGAM out-performance falls shy of the pace and magnitude recorded during this stage of the epic 2015 FANG run; this is reflected in the graph above and in the left-panel charts in the pdf link below. The right-panel charts telescope more granularly into their YTD CAR.

Shown between the charts is the recent CAR trend (trailing 5d, 10d, 15d, 20d & 25d) to transmit second-order CAR behavior and, at the risk of transmitting false signals, a qualitative signaling label based on the recent ST CAR trend (using a rules-based algorithm to quantify the qualitative labeling process).

Finally, as a caveat, it is important to note that these are highly noisy processes with the potential for false-signal whipsaw and with the magnitude and horizon/phase length subject to tremendous variability; the analogy might be RSIs which can stay extended for long periods of time with the magnitude of subsequent mean reversion quite uncertain.

Note: calculations Risk Advisors, data Bloomberg

Proprietary and confidential to Risk Advisors