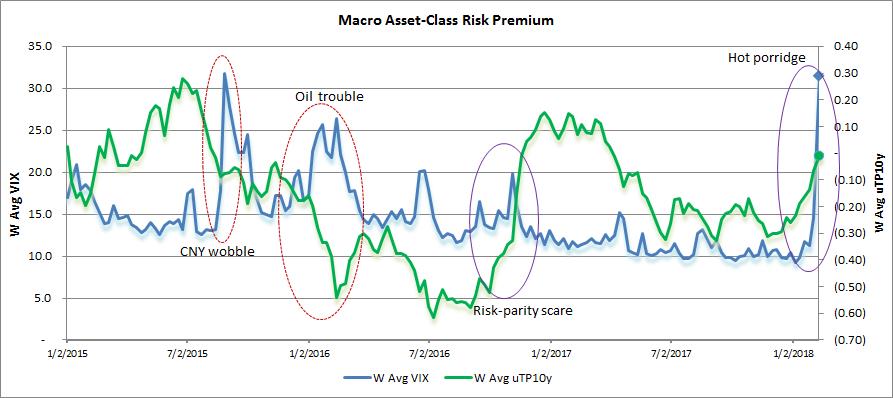

Punch line: following the recent “Macro asset-class risk premium” post, the below chart updates the recent stock-bond risk-premium (VIX/term premium “uTP”) dynamic, perhaps reminiscent of the winter-2016 inflation-driven risk-parity scare when both rose in unison (S&P 500 episodic drawdown: -4.8% Aug 15, 2016 to Nov 4, 2016 vs. -10.2% Jan 26, 2018 to Feb 08, 2018 ). Stay tuned!

Note: calculations Risk Advisors, data Bloomberg

Proprietary and confidential to Risk Advisors