Punch line: over the past year the S&P 500-USD relationship on average appears quite random. However, this aggregated data belies the forceful regime behavior (traditional FX: S&P 500 +ve/-ve while USD -ve/+ve vs. pro-growth: S&P 500 and USD +ve/-ve in tandem) that has frequently prevailed beneath an overall ambivalent hood. Further, regime-conditional industry sensitivity was asymmetric for several industries.

Given the recent flux in the S&P 500 (SPX)-USD (proxied by DXY) relationship I took a look at its evolving behavior over the recent past partitioned by correlation regime: traditional FX regime (SPX +ve/-ve while DXY -ve/+ve) where trade-competitiveness/currency-translation dynamic hold sway vs. pro-growth regime (SPX and DXY +ve/-ve in tandem) where growth and growth-differentials color both concurrently.

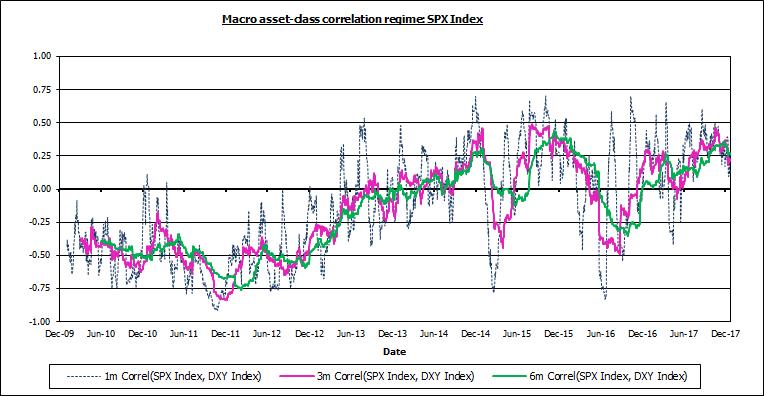

The time-series chart below frames the analysis by tracing the SPX-DXY moving-average correlation from Jan 1, 2010 (post GFC drawdown and aftermath) to date. As the chart attests, there have been forceful and protracted instances of traditional FX as well as pro-growth behavior. Coming out of the GFC correlation was -ve highlighting the traditional FX regime. Later, as the recovery cemented, correlation moved +ve underscoring the pro-growth regime. Typically, traditional flight-to-safety response sees the SPX and DXY move inversely whereas during the Draghi-reflation episode, the Euro became a carry-trade funding currency, safe-haven flows frequently saw SPX-DXY move in concert as carry trades were unwound.

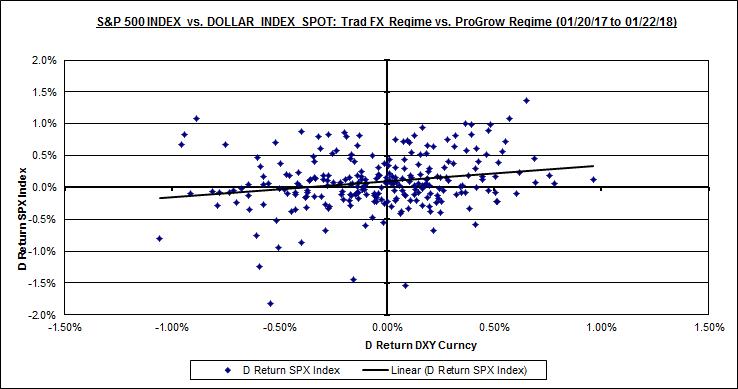

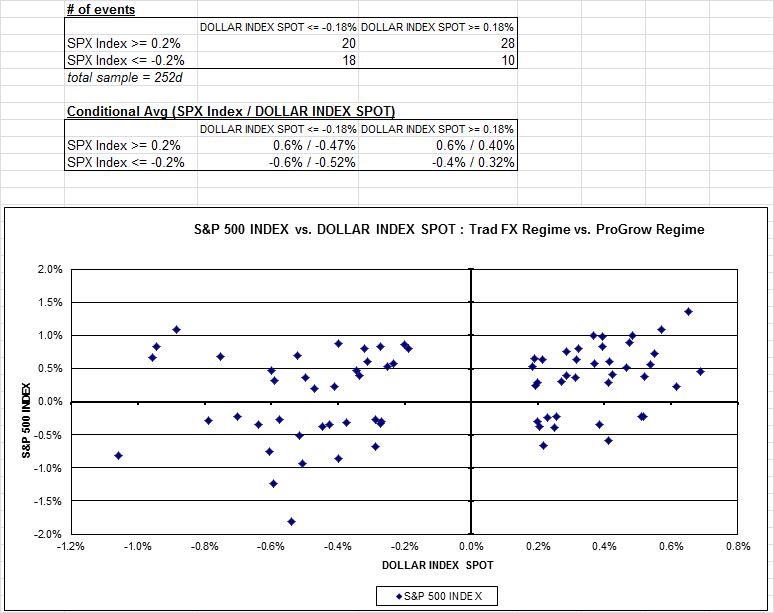

Telescoping to the past year, the scatterplot below shows that the SPX-DXY co-movement dynamic has on average been fairly random.

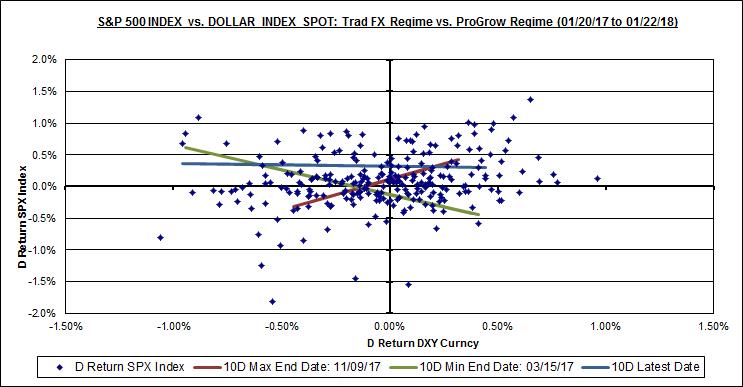

However, this aggregated data belies the more forceful regime behavior that has frequently prevailed, in the ST, over the year past. The chart below superimposes the most forceful instances of ST regime behavior via their piece-wise regression lines, statistical-significance notwithstanding. The brown line reflects the pro-growth regime prevalent during the 10d ending 11/09/17 (correlation +0.8) and the green line depicts the traditional FX regime prevalent during the 10d ending 03/15/17 (correlation -0.9). The blue line portrays the random relationship over the most recent 10d.

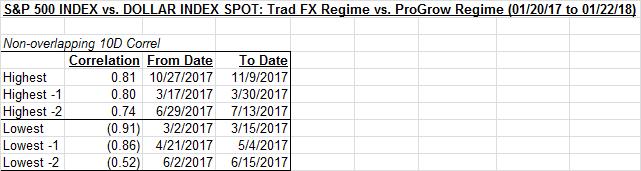

As illustrated in the table below, using 10d non-overlapping windows over the past year, there have been multiple instances of forceful SPX-DXY behavior in either direction.

This message, of forceful regime episodes beneath an overall ambivalent hood, is further reinforced using “significant” SPX-DXY days: SPX >= +/- 20bp and Euro >= +/- 18bp (both 0.5-sigma thresholds). The table and chart below illustrates that all four quadrants are well populated, though the pro-growth +ve quadrant (SPX and DXY +ve) dominates. More granular detail is provided in the attached pdf.

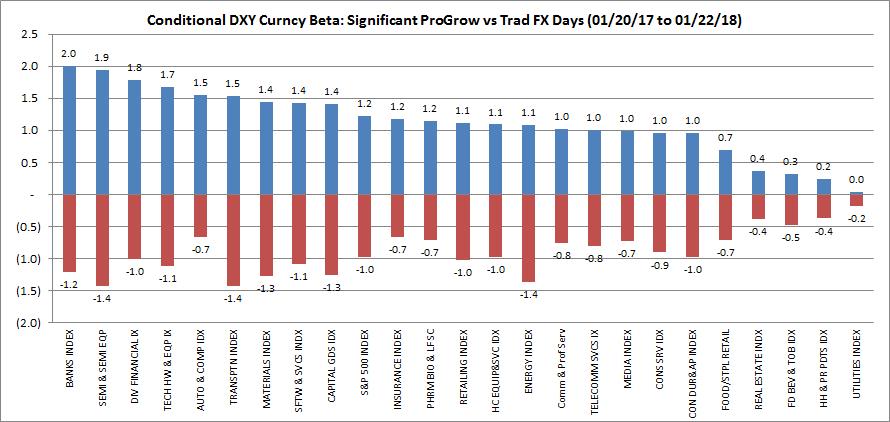

Regime- and “significant”-day conditional industry sensitivity:

Next, I looked at the industry sensitivity, as measured by conditional beta, using the “significant”-day criteria and segmented by correlation regime. Majority of industries, as reflected in the chart below, had fairly symmetric betas to the DXY, conditional on the correlation regime. Others, particularly towards the left wing, had asymmetric relative betas, which highlights that magnitude of industry sensitivity to the DXY, not just sign, was contingent on the underlying equity-currency correlation regime. For instance, banks, diversified financials and insurance; semis and tech hardware; and autos had large +ve pro-growth regime betas and more muted –ve traditional FX regime betas, likely reflecting greater implicit pro-cyclical rate sensitivity. Interestingly, energy and materials displayed fairly symmetric betas, despite their purported inverse-$ proclivity. This is portrayed in the chart below:

In summation, this analysis underscores that the equity-currency relationship is fraught with imprecision and enhanced basis risk; not just the magnitude of the sensitivity but the sign as well.

Note: calculations Risk Advisors, data Bloomberg

Proprietary and confidential to Risk Advisors