Punch line: Q1, 2017 S&P 500 sector returns were mostly firmer contributing to a healthy index gain. Sector returns were led by secular-growth tech and lagged by energy. Intra-sector stock-returns were well dispersed within several sectors including consumer discretionary, healthcare and tech, with other sectors, including energy and financials, sporting tight groupings. These are reflected in the charts and tables below.

The following is an update of the quarterly sector-level dispersion analysis which reveals mostly firmer sector-level performance and varied intra-sector dispersion outcomes:

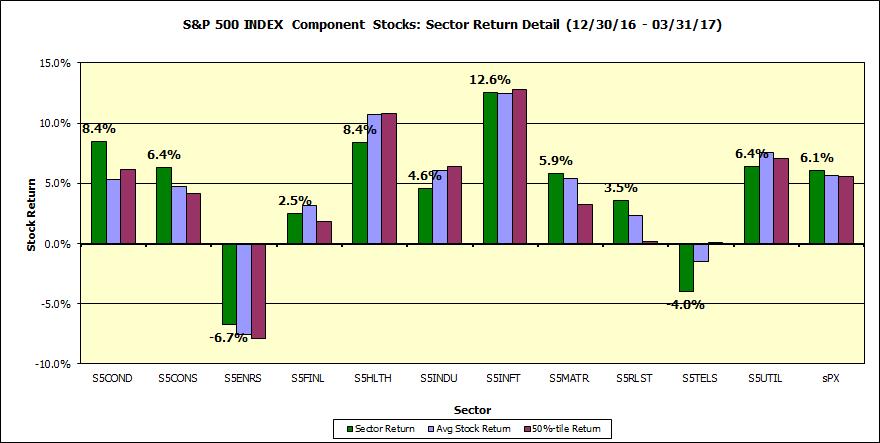

This first chart notes the sector (cap-weighted) return (green bars), average (equally-weighted) return (blue bars) and median stock return (burgundy bars) for the various sector of the S&P 500 over the Q1, 2017 horizon (with dividends, latest constituents). Sector returns were mostly firmer led by secular-growth tech with energy and telecom services the sole two laggards. At the index level, and for several sectors, cap-weighted returns bested equally-weighted returns reflecting large-cap outperformance within the S&P 500.

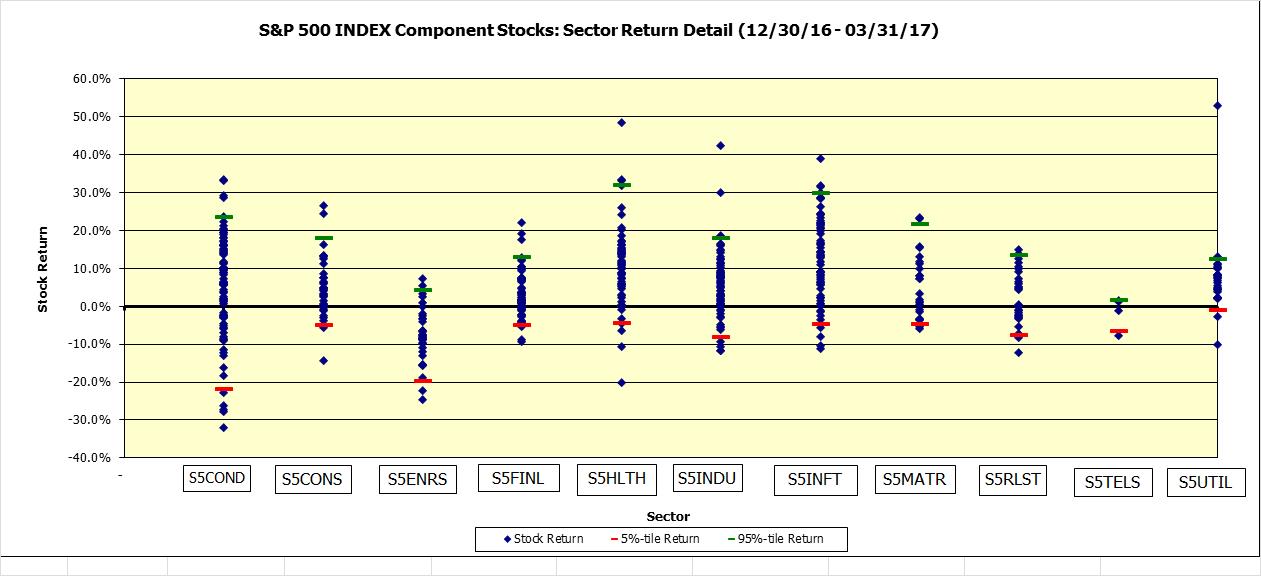

Next, a scatter plot of stock returns by sector, along with 5%- & 95%-tile markers. Intra-sector stock-returns, relative to their volatility, were well dispersed within several sectors including consumer discretionary, healthcare and tech, with other sectors, including energy and financials, sporting tight groupings.

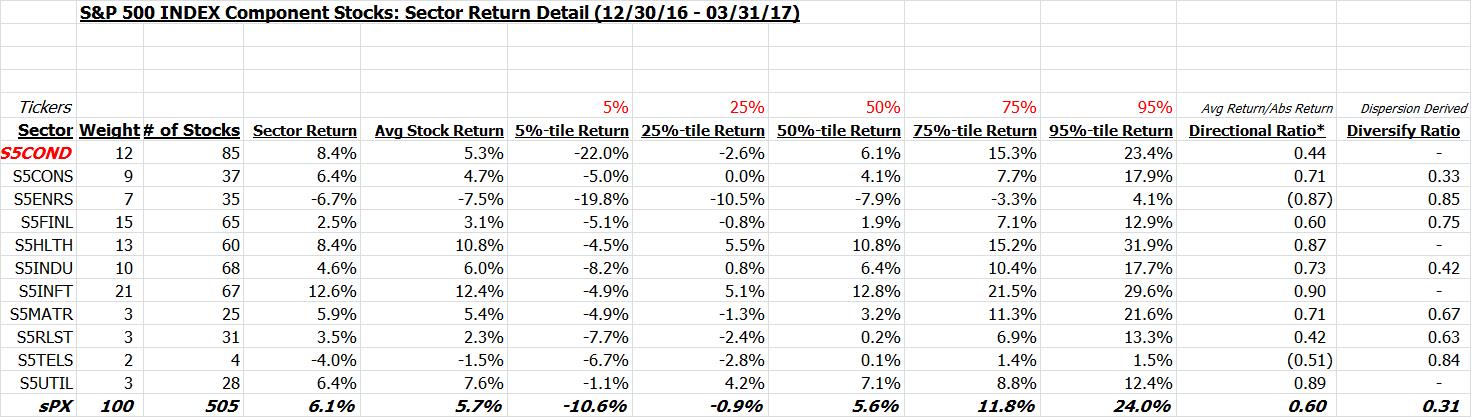

This is also shown in tabular form along with the %-tile sector return distribution. Also shown are the directional ratio (avg net return to avg gross return) and dispersion-based diversification ratio (~ equally-weighted index vol/component vol), both of which point to differential sector outcomes.

Finally, a listing of stock returns, by sector, ranked in descending order of performance is shown in the pdf link below:

Stock by sector returns Q1, 2017 PDF

And, very finally, the cumulative abnormal return (“CAR”; summation of daily beta-adjusted excess return) of the S&P 500 GICS industries, over the Q1, 2017 horizon. I ran the CAR for each S&P 500 industry, sorted them in descending order of outperformance, and charted the top 10/bottom 10 CAR industries in the below pdf links.

CAR Industry BOTTOM Q1, 2017 PDF

Note: calculations Risk Advisors, data Bloomberg

Proprietary and confidential to Risk Advisors